|

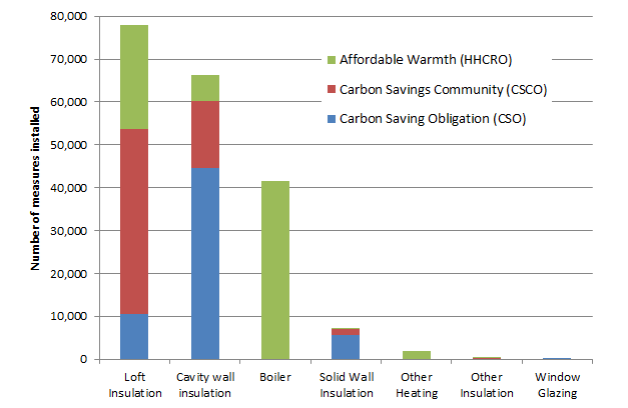

A lot has been made in the media and in politics that the Green Deal has not taken off and there are suggestions from some quarters that it should be scrapped. Readers of this blog will know about my own criticism and issues encountered with the Green Deal for my own house. So far there are ’12 Green Deal Plans’, which I understand are the households currently having had their measures installed, but 677 were in the system since the end of August. This would exclude our GD plan and many others presumably. As time progresses, more plans will have been installed; but these numbers are still in stark contrast with the 71,000 GD assessments so far undertaken. Though this disjunct may be partially explained by the fact that the figures above do not include householders choosing to act outside the GD. More impressively however is that by the end of July there had been ~ 196,000 ECO measured installed, benefiting 173,000 households. Most of this was loft insulation(40%), cavity wall(34%) and boiler upgrades(21%) with just 4% solid wall insulation installations, as is illustrated in DECC's graph below.  ECO measures installed by end of July 2013 - by DECC Reducing carbon emissions associated with domestic space heating is a key aspect to meet the UK Government’s overall emission reduction targets of 80% from 1990 levels by 2050 (Crown, 2008). Given that 7.8 million of 26.7 million dwellings in Great Britain are solid walled dwellings (DECC, 2012) and roughly 98% have un-insulated walls (DECC, 2012); the number of solid wall installations is particularly disappointing. To meet the ambitious carbon reduction targets set by Government in the Climate change Act, almost all such dwellings will need to be upgraded, yet while ploughing through literature, it struck me how little we actually know about the existing housing stock, and in particular pre-1919, solid walled dwellings. The STBA (May, 2012) highlight the lack of knowledge and the potential increased risk for unintended consequences to occur with damage to the building fabric, if we are not careful. Gauging from industry interest in my own PhD research on pre-1919 suspended timber ground floor heatloss and insulation measures, I am aware that industry will need answers much faster than the time it takes to collect evidence. Perhaps the slow green deal uptake is a blessing in disguise? Rather than rolling out measures on a large scale, there is the benefit of a slower uptake to learn lessons and for industry and academia to collect evidence of associated risks and how to minimise them. References: CROWN 2008. Climate Change Act 2008: Elizabeth II ( Chapter 27) 2008. Great Britain: The Stationary Office Limited. DECC 2012. Statistical release: Experimental Statistics; Estimates of home insulation levels in Great Britain: January 2012. In: CHANGE, D. O. E. C. (ed.). London: Department of Energy & Climate Change. MAY, N., RYE C 2012. Responsible Retrofit of Traditional Buildings. A report on existing research and guidance with recommendations by STBA.

0 Comments

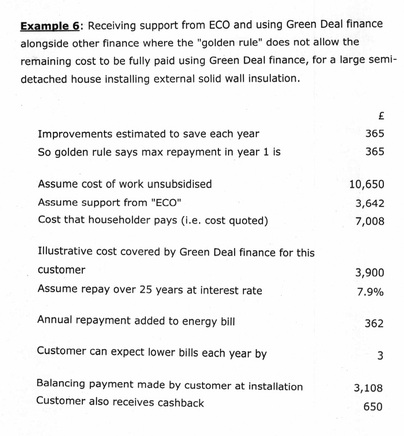

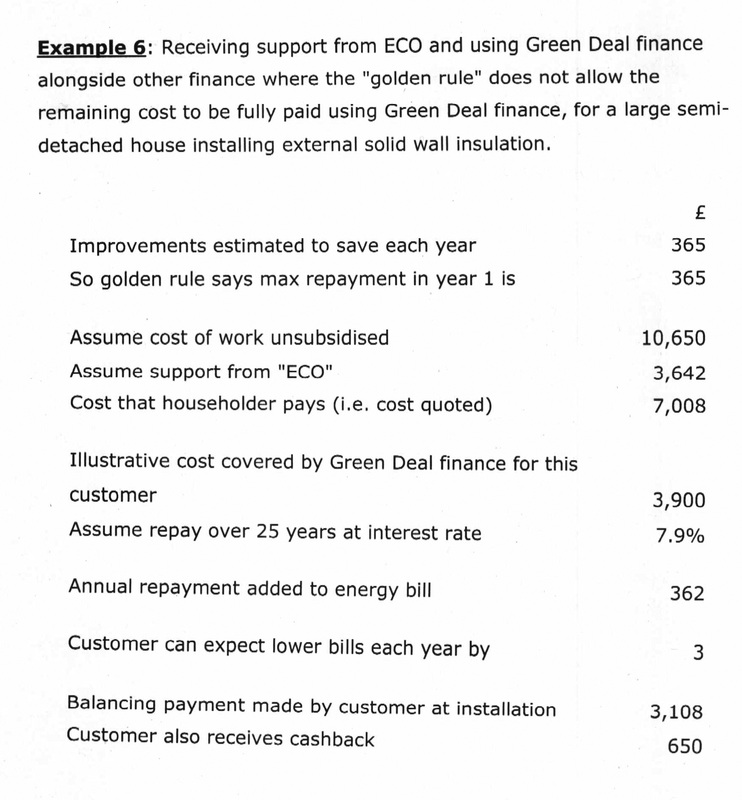

This blog post is inspired by an email from Stewart Gilmour, CIBSE Director of finance and Services, quoting the Chief executive of the Green Deal Finance Company (GDFC) Mark Bayley who said the interest rate was very competitive already: “If you take a typical finance for a boiler over several years, you are looking at 19% and ours is less than 9%.” Compared to the Bank of England base rate of 0.5%, 9% does not sound competitive at all, does it? In Germany, a similar 'pay as you save' scheme as the Green Deal was hugely successful with the energy-efficient improvement of about 1 million existing homes between 2006-2009. It achieved this with low interest (subsidised) loans and performance targeted subsidies (full report by UCL Energy Institute and LSE here). The interest rate was 3-5% fixed rate for ten years, and no early redemption penalties. Given the high quoted Green Deal interest rates and the difficulty to get a Green Deal Finance Plan, we decided to try to finance our GD interventions another way (i.e. part savings, part personal loan). We cannot remortgage before 2016 as we are in a fixed rate, so we cannot release 'cheap' money this way like some others can; nor does our bank offer a low interest rate loan for energy efficiency improvements, as offered by Nationwide at below 3% interest rate for existing mortgage holders. Yet Bayley may not have been so incorrect stating that the 9% rate is "competitive". While many advertised bank loan rates are around 5-6% (assuming good credit; more like 14-15% with fair credit); the less money you borrow, the higher the interest rate. For example, if you do not hold a Nationwide mortgage and are borrowing with a standard personal loan instead; < £5000 from Nationwide will attract 11.9% interest; while between £5000 and < £7500 this is 8.9% and the lower advertised rate of 4.9% does not kick in until you borrow > £7500. Most loans work this way. And these are quite good rates for small amounts of money, for example the Bank of Scotland's rate for < £5000 is as much as 19.5%; though the cheapest I could find for this amount was Zopa (peer to peer lending) with 6%. With personal loans, the payback is usually ≤ 5 years, while for the Green Deal this can be spread over a longer term, with a minimum of 10 years, ofcourse building up proportional interest accordingly (see later). As this is paid back through the energy bills, selling your house would in effect pay off 'your' loan, by passing it to the next homeowner with the house sale, unless you need to pay it off early to find a buyer; there are likely to be early repayment redemption penalties for GD loans. Example 6, courtesy of DECC*, below highlights that repaying £3900 over 25 years at an assumed interest rate of 7.9%, will result in a total cost to be paid back of around £9000, with £362 annual repayments, or around £30 per month. However, if you can afford a higher repayment of £85 per month, you are better off taking the Nationwide loan, even at nearly 12%, as you'd paid back a total of £5100 after 5 years for the initial borrowed £3900.  So, is the 9% Green deal rate competitive? Depends how you look at it and what other access to money you have and how much you can afford to repay each month. It is indeed a good thing that there are other incentives to bring costs down for those on low incomes. As our Green Deal Assessor said at her visit: "you may find that borrowing under the Green Deal Finance Plan is not the best way to fund the improvements, so look around." This advice is sound, it seems! * As stated on first page; these examples are for information only and not for financial advice. All 6 examples below. A quick update: the third installer called me earlier in the week to see if we wanted to go ahead. I reminded them that in addition to some more detail on their quote we still had not received any ECO-funding offer.

They - surprisingly - told me that I should get this through the provider, not them. I told them that this is not what other installers have done; nor what I understand needs to be done, and that I was asked for the EPC.Xml file for them to work it out. They called me again today saying that the EPC.xml file - which I sent more than 2 weeks ago - does not seem to work with their IT system and would I mind that they would come and do another Green Deal assessment, free of charge? I told them they were welcome to do so, but that it likely would be a waste of their time: we received a good quote from installer 1; who can also do the roof for us and we are looking to work with them. I also told them the quote is only valid till the end of the month, and I was not confident they could give us a quote in time. They decided to not proceed with another assessment. I politely gave them some more constructive feedback about their process, but I am not sure how much this was appreciated! Courtesy of Linn Rafferty - here is a list of providers who offer Green Deal finance. Though it is unclear how many constraints there are to them considering finance. For example, you may need to live in a certain area, be eligible for ECO/benefit etc. British Gas for example told me that they do not work with individual householders at this stage. Any more stories out there?

At the time of writing (Sept 1st) it has taken me almost 6 months from Green Deal assessment through to having obtained 2 Green deal quotes, setting out any ECO funding for external wall insulation (EWI). I contacted over 40 providers in March, many of whom did not respond; and those that did, said they were not yet ready to deliver the Green Deal Finance or did not deal with individual owner-occupiers. Thanks to DECC I had Instagroup, who have access to ECO-funding for individual householders on behalf of EON, get a Green Deal approved installer to get in touch with me. Let’s refer to them as Installer 1.

From a very helpful blog-reader I also received the contact details of another installer (let’s call them Installer 2) who have ECO funding access, though could not yet offer the Green deal Finance and worked with a Hanson system. They charged £60 for a surveyor to come out, and I was ensured I would obtain a quote for the works within a few weeks from their visit. Installer 1 however failed to show the first time round; Instagroup were apologetic and gave me details of Installer 3 and 4. We also had Parity Projects visit us as part of their pilot in Haringey for their Green Deal Conduit scheme'. Meanwhile, Installer 1 showed up (late!), but I was impressed with the visit undertaken, and the respectful attitude and helpfulness overall. For example, they talked us through how the works would be done; mentioned thermal bridging, what the system is like (thickness/what happens to window reveals etc). Most importantly of all, this installer was also open to insulating our flat roof and waterproofing it at the same time, and recognised this would be ideal done together with the scaffolding up and to have a neat wall/roof junction. Installer 2 and 3 refused to do it, not even engaging with a sub-contractor. (NB: Installer 4 never called me back after giving initial details) Installer 3, aside from refusing to insulate the roof (“we are an insulating firm, we insulate pitched roofs but do not do any waterproofing”), also plainly refused to consider any works to the front facade. Their reasoning was that for EWI, it is “too complicated and requires planning” (no, it does not for our property, as far as I am aware). They also would not consider internal wall insulation. At all. (“Too much hassle”). They also made the briefest of all visits, and did comment that they found that they had a lot of interested people but occupants were not going ahead due to costs still being too high, even with ECO. Installer 1 eventually made a total of 3 visits: one was from a GD assessor, whose software had immediate access to the ECO-funding provided by their provider. There was no need for an Occupancy Assessment, as we would not be seeking Green Deal finance (and he had our previous one in any case). He also input the back ‘extension’ separately (although built at the same time as the rest of the house) as he was surprised that flat roof insulation was not originally listed as an approved measure in the first assessment. Interestingly, it did now come up as an approved measure. A third visit was with the roofing subcontractor to assess the flat roof and how to best insulate it. A few interesting things have come out of this process: 1. Competitive edge: The companies most flexible to meet the customer's requirements are likely to have a competitive edge: the fact that the roof can be done at the same time with least hassle to us, was definitely driving our decision who to work with, before we knew the ECO-funding available. 2. ECO-funding: The amount of ECO- funding was surprisingly different. This is obviously also a big driver. Please see below. 3. BBA approval: Chasing installer 1 and 3 for their quotes, Installer 1 informed us that the delay is caused due to BBA approval, which is required under the Green Deal. They explained that the system they were using had to be changed from PIR to EPS insulation and that - disappointingly- reveals would no longer be treated.(previously aerogel + render finish to reveals) 4. Quote from Installer 2: as they had promised, within 2 weeks we received a detailed description of the works with 2 quotes (each specification around 12 pages long): a quote for insulating both front + back and one quote to insulate just the back. The ECO ‘grant’ is deducted clearly on the ‘acceptance letter’ supplied. As explained in point 9 below, we will likely only get the back insulated under the Green Deal. The quote for the back elevation, amounts to ~ 25% ECO- funding of the EWI cost. The quote is valid for 2 months and uses a Hanson system. 5. Speedier quotes if no access to Green Deal Finance required: Work by Installer 2 works out at a total of around £4700 including VAT (reduced with ECO-funding) for insulation to the back of our terraced house. It is at this point we realised we may be able to fund this work through other means, and we would probably not need access to Green Deal Finance. We informed Installer 1 and 3 that we were now just looking for access to ECO-funding and no longer GD finance, and quotes materialised in a matter of weeks. However, in either case this - frustratingly - excluded any detailed breakdown (just 1 x A4) and no ECO-funding. It is at this point of asking for more detail and exact ECO-funding, that Installer 3 informs me that they need the EPC.xml file. Within a week, the original assessor had supplied this to me, however I have yet to receive a quote several weeks later. It also seems that Installer 3 is supplying a Saint-Gobain EWI system now. 6. Installer 1 quote: Installer 1, at this stage our preferred installer, offered the cheapest cost for the EWI, perhaps because the job had become bigger for them with the roof in addition? I addition, the ECO-funding they have access to, would cover around 65-70% of the cost of the EWI. Basically, we can now afford to install EWI to the back plus roof insulation, without having to access Green Deal finance (though we probably still need to borrow part of it from somewhere else). The quote expires after 1 month. It is due to this reason, that unfortunately we will no longer be able to be part of Parity Projects' Green Deal pilot scheme. 7. Green Deal Quality control: Installer 2 made mention that < 90mm systems are available for the front facade, utilising phenolic foam. However due to potential movement joints leading to cracked render over time, caused by loss of density of the foam, this is not offered under the Green Deal as it is not approved/not warrantied for 25 years (you can get it under the Green Deal with brick slip finish however as the cracking does not occur). This is reassuring - though one important question: why offer it at all outside the Green Deal if these are the associated issues? 8. Confidence & trust: Installer 2 supplied a detailed breakdown of all the works and warranties, which instills confidence. I have yet to receive this from any others, including Installer 1, whom we have decided to work with. I did however email lots of detailed questions to understand what was/was not included before making a decision. However I prefer to obtain a detailed listed quote as we did from Installer 2, before going ahead. On the other hand, I also appreciate that this is time-consuming and ‘at risk’ for each installer to undertake for each potential customer. Ultimately, we do feel that a level of trust and understanding has built up with Installer 1 - hopefully this materialises as we proceed to the next stage. 9. EWI system design & performance: It is a shame no system seems to include treatment to window reveals, or a satisfactory solution to the front facade. Not insulating the reveals increases surface condensation risk and will reduce the overall performance of the wall, below it’s intended 0.3W/m2K. With regards to the front facade: ECO-funding can only be obtained by upgrading to Part L (0.30 W/m2K). To the front, this means 90 mm of insulation: this will look very strange on a front facade in a set of terraced houses. In addition, the bay window would not be touched, leaving stone work uninsulated and stone cill supports would protrude out of the 90 mm insulation - all of which would just make for bizarre detailing. Installer 1 conceded none of this is ideal. Anyone out there with any great ideas or suggestions/examples of how this can be done? Installer 1 will continue to look at this too. 10. Time: Finally, the whole process of obtaining quotes, allowing time for visits and following the installers up on an almost weekly basis to keep pressure on them about ECO-funding has been much more time consuming than anticipated. However, it has been worthwhile getting more than 1 quote. The ECO-funding available will change from provider to provider and from install to install as well as over time. The difference of ECO-funding between Installer 1 and 3 may be explained perhaps by the fact that they are attached to different providers or that there was nearly 2 months between quotes? The fluctuating nature of the level of ECO-funding may also perhaps be illustrated by Installer 1 offering just a 30 day validity of its quote. It has taken almost 4 months from assessment to the first Green Deal quote with ECO-funding, and almost 6 months to have at least another quote. And this includes a lot of effort at my end, and initial intervention from DECC to get it kick-started. To be honest I had not envisaged this, and I thought we would have had the works done by now. No measures are installed yet and I am not sure when they will, so I am not surprised that ‘only’ 132 of some 58,000 assessments signed up. On the other hand, the Green Deal is a new scheme and everyone is still finding their feet, so let’s hope more of these assessments materialise in actual improvements n the following months. I will keep you posted on progress and process in the meantime! On another note: Several people have contacted me about access to ECO-funding for individual householders. Contact Instagroup (0118 932 8811 or 0800 0517420) Say you'd like to speak about GD in your area - they should then put you through to a local area manager who then has details of local installers to come around and asses the property + let you know what ECO funding is available. The other company able to access Green Deal ECo funding is Hanson. Next - Green Deal Cashback: I am not sure if we qualify for a cash back or how to apply for it. The following links may also be of interest to readers of this blog:

|

About SofieThis is Sofie's blog; or rather a collection of musings & articles sometimes also published elsewhere. More about Sofie here. Archives

April 2014

Categories

All

|

RSS Feed

RSS Feed